This includes indirect labor costs, which are labor costs incurred by a company for those employees who are not directly involved in producing the actual good. Examples of employees in this category are managers, nurses, security guards, janitors, cooks, maintenance workers, accountants, executives, trainers, parking attendants, and secretaries. We used this formula to calculate conversion costs, but it can also be used to find one of the missing variables, such as direct labor costs or manufacturing overhead costs. From this, we can set our price, fill in our balance sheet, and complete our income statements.

How to Calculate Conversion Cost Formula Example

The contribution margin per unit of conversion cost is the difference between the selling price and the variable cost (including direct materials and variable overhead) divided by the conversion cost per unit. In this section, we will delve into the concept of Conversion Cost Variance and explore how it can be measured and analyzed. Conversion costs refer to the expenses incurred during the transformation of raw materials into finished goods. Identify the direct labor and manufacturing overhead costs for a given period. Direct labor costs are the wages and benefits paid to the workers who directly work on the product. Manufacturing overhead costs are the indirect costs that support the production process, such as utilities, rent, depreciation, maintenance, etc.

Related AccountingTools Courses

Therefore, once the batch of sticks gets to the second process—the packaging department—it already has costs attached to it. In other words, the packaging department receives both the drumsticks and their related costs from the shaping department. For the basic size 5A stick, the packaging department adds material at the beginning of the process.

Manufacturing overheads:

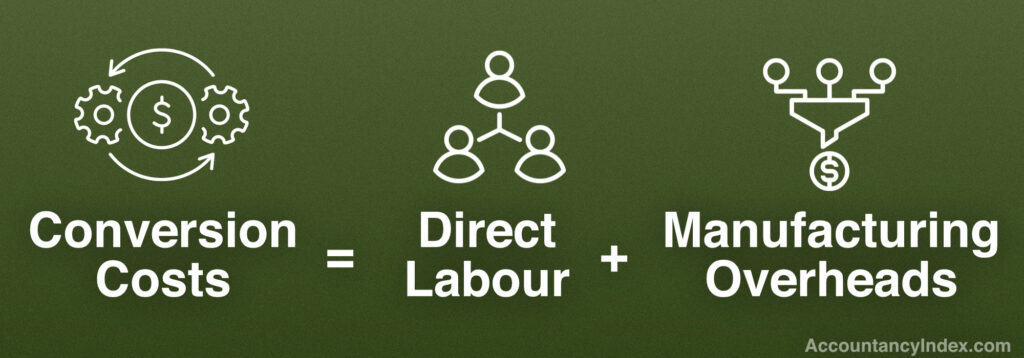

In this section, we will delve into the concept of the conversion cost ratio and its significance in cost accounting and management. The conversion cost ratio measures the proportion of conversion costs to the total manufacturing cost, providing valuable insights into the efficiency and cost-effectiveness of the production process. Add the direct labor and manufacturing overhead costs to get the total conversion cost for the period. For example, if the direct labor cost is $50,000 and the manufacturing overhead cost is $40,000, the total conversion cost is $90,000. Conversion Cost is the total money a company spends to transform raw materials into finished products. It includes direct labor (workers’ pay) and manufacturing overhead (other production expenses).

- In a processing environment, there are two concepts important to determining the cost of products produced.

- Managers can view this information on the importance of identifying prime and conversion costsfrom Investopedia, a resource for managers.

- The conversion of materials into a finished product is what we call “conversion.” It’s an important process that happens at every stage in the manufacturing cycle.

- As can be seen from the list, the bulk of all conversion costs are likely to be in the manufacturing overhead classification.

- Examples of manufacturing overhead include the utilities, indirect labor, repairs and maintenance, depreciation, etc. that is occurring within a company’s manufacturing facilities.

A positive variance indicates that the actual conversion costs exceeded the budgeted costs, while a negative variance suggests that the actual costs were lower than the budgeted costs. This means that the toy company spends $10 on direct labor and manufacturing overhead for each doll it produces. This means that the company spent $9 on converting each unit of the product. This information can be useful for cost accounting and management purposes, which we will discuss in the next topics. A periodical review of the firm’s prime cost is crucial to ensure the efficiency of its manufacturing process.

Conversion Cost vs Prime Cost

The more complex and sophisticated the products become, though the higher this cost can potentially go up. The use of this ratio in process costing is to calculate the cost for both direct labor and manufacturing overheads. It’s important because it will become the cost of the inventory which will impact the selling price. In a typical manufacturing process, direct manufacturing costs include direct materials and direct labor.

By comparing the actual conversion cost with the budgeted or standard conversion cost, managers can identify the variances and the causes of them. Indirect materials, electricity charges and salaries of engineer and supervisor are all indirect costs and have, therefore, been added together to obtain total manufacturing overhead cost. Conversion balance sheet items items of balance sheet with explanation costs only include direct labor and manufacturing overheads because of the reason that these two variables are rudimentary to execute the overall process. Let’s consider an example to illustrate the concept of conversion cost variance. Suppose a manufacturing company budgeted $100,000 for conversion costs for a particular production run.

However, they may also include the cost of supplies that are directly used in production process, and any other direct expenses that don’t fall under direct materials and direct labor categories. Direct material and direct labor costs are prime cost because they are the main incremental costs of a product. The greater the proportion of prime costs in total costs of a product, the more reliable is the cost estimate of the product. Conversion costs are the costs that are incurred in converting direct raw material into finished goods and hence the name. The conversion cost is reported in the financial statements as part of the COGS and the inventory valuation. The cogs is the cost of the goods that are sold during the accounting period, and it is deducted from the sales revenue to calculate the gross profit.

As can be seen from the list, the bulk of all conversion costs are likely to be in the manufacturing overhead classification. In a business that uses a high degree of automation, it is likely that manufacturing overhead costs will comprise the bulk of all conversion costs. In the Peep-making process, the direct materials of sugar, corn syrup, gelatin, color, and packaging materials are added at the beginning of steps 1, 2, and 5.